This is because we assess each of our securities as objectively as possible. It is an imprecise exercise, but one that I consider essential. We update these assessments quarterly, following the release of results for each of our businesses.

Although we are long-term investors, our assessment of a security is based, among other things, on the earnings forecast that we make for the coming financial year. I don’t like making predictions (especially those concerning the future!), but you have to look a little ahead when evaluating a company.

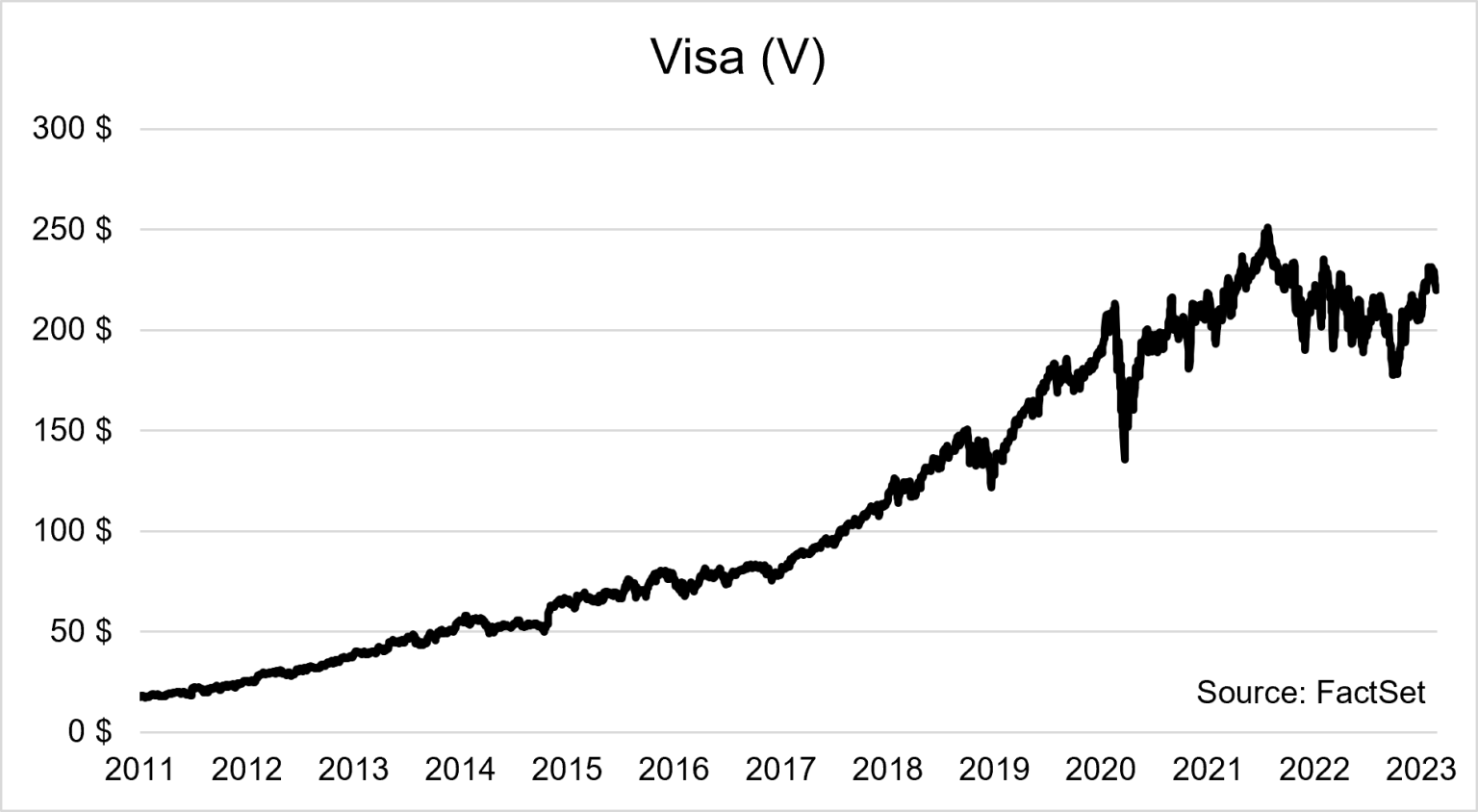

However, it often happens that the price of a security that we own exceeds our valuation. As an example, we have owned shares of Visa (“V”) since 2011. Except for the period when we initially acquired it, the stock has rarely sold below our valuation. If we had sold the stock when its price exceeded our valuation, we would not have held it very long and we would have lost a lot:

Fortunately, we never sold our Visa shares (or only partially).

This is a good example that makes me repeat that we should be patient with the securities of quality companies whose growth potential remains attractive over the long term.

A valuation is not precise and it is a “moving target”. Thus, the share price of a growing company such as Visa will tend to increase from quarter to quarter, from year to year, according to its growing profits. Over the past 12 years, our valuation has risen almost continuously, based on steadily and rapidly growing earnings.

So, when a quality stock outperforms its valuation, I suggest trying to look beyond the next year. What might the company’s profits be in three or even five years? Certain growth assumptions are made for the coming years, while remaining realistic and conservative.

Does the stock still seem too expensive based on possible earnings in five years? If so, a partial (perhaps even full) profit taking could be considered. But, unless a quality stock like Visa becomes excessively expensive, I recommend sticking with it.

A completely different decision concerns the securities of companies whose financial performance has been disappointing for several quarters. Or whose business model we believe has become less attractive, either due to strategic decisions by its management or pressure from its competitors. Or whose level of risk we judge has become too high, for example, due to a sharp increase in its debt. In such cases, one should be much less patient.

This is what I call patience at two speeds.